Guides

Lease vs Buy a Car in Albania: Make the Right Choice

Lease vs Buy a Car in Albania: Make the Right Choice

TL;DR:

- Choosing whether to lease or buy a car in Albania depends on your usage, financial goals, and understanding of total costs. Leasing offers lower monthly payments but limits ownership and adds mileage and wear restrictions, while buying involves higher upfront costs but builds equity over time. A thorough comparison of total ownership expenses and careful contract review are key to making the right decision.

Choosing between leasing and buying a car in Albania can feel like navigating a maze while someone keeps moving the walls. You see a lease advertised with low monthly payments and think it looks great, then you wonder what happens at the end of the contract and whether you walk away with nothing. Or you consider buying outright and suddenly face a large down payment, financing rates, and the long-term responsibility of owning an asset that depreciates the moment you drive it off the lot. This guide cuts through the confusion by walking you through total cost comparisons, contract fine print, and a practical decision framework built around Albanian market realities.

Table of Contents

- Understanding the difference: Leasing vs buying

- What you need to compare: Total cost calculation

- Step-by-step: Deciding for Albanian car buyers

- Troubleshooting and common mistakes to avoid

- Our perspective: Lease vs buy in Albania isn’t a one-size-fits-all answer

- Explore your options with CarPulse

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Total cost matters most | Compare all upfront, monthly, and contract-end costs to choose the best option. |

| Contract fine print counts | Read lease agreements carefully for mileage limits and fees that impact overall value. |

| Equity and flexibility | Buying builds long-term equity and allows flexible usage beyond lease terms. |

| Local market realities | Use calculators and stress-test assumptions with Albanian rates and usage patterns. |

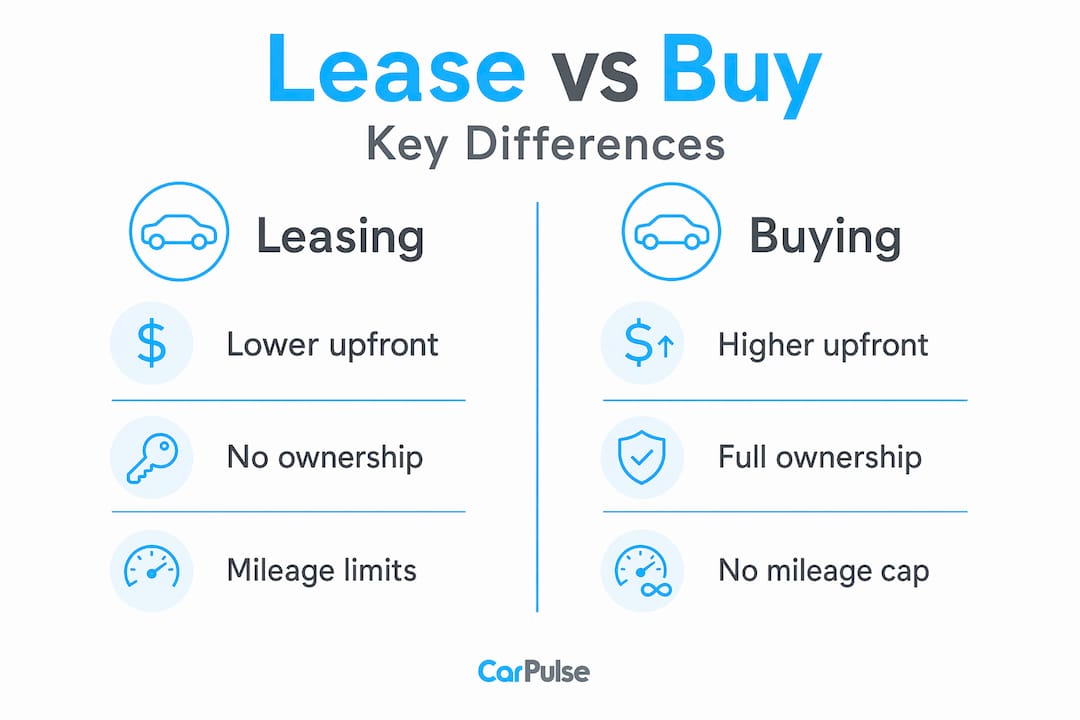

Understanding the difference: Leasing vs buying

Before you can make a smart decision, you need to know exactly what you’re comparing. Leasing and buying are fundamentally different financial arrangements, even though both put you behind the wheel of a vehicle.

When you buy a car, you own it outright, either by paying cash or taking out a loan. Once the loan is paid off, the car is yours with no further payments. You can modify it, sell it, or keep it for as long as it runs. When you lease a car, you’re essentially renting it for a fixed period, typically two to four years. You make monthly payments, return the car at the end of the term, and start over. As leasing and buying differ materially in ownership, upfront payments, monthly payment structure, usage restrictions, and equity build-up, the two paths lead to very different financial outcomes.

Here’s a quick side-by-side to make those differences concrete:

| Factor | Leasing | Buying |

|---|---|---|

| Ownership at term end | No (return car) | Yes (fully yours) |

| Upfront costs | Lower (first payment, fees) | Higher (down payment, taxes) |

| Monthly payments | Lower | Higher |

| Mileage restrictions | Yes (typical: 15,000 km/year) | None |

| Equity built | None | Yes, as loan is paid down |

| Modifications allowed | Usually not | Yes |

| End-of-term flexibility | Limited | Full |

Monthly payment differences between leasing and buying are often more dramatic than buyers expect. Understanding auto loan payment differences early prevents you from comparing figures that aren’t measuring the same thing. For Albanian buyers exploring car financing in Albania, it’s worth noting that the local financing landscape for leasing is still maturing, which means contract terms can vary widely between dealerships.

Key leasing restrictions you must know before signing:

- Mileage caps: Most lease contracts set a maximum annual mileage, and going over that triggers per-kilometer penalties.

- Wear-and-tear standards: Normal wear is expected, but damaged upholstery, scratches, or worn tires beyond defined limits cost you money at return.

- Early termination fees: Ending a lease before the agreed term is expensive and sometimes not even allowed without significant penalties.

- Modification limits: Tinting, accessories, or mechanical modifications typically void lease terms.

What you need to compare: Total cost calculation

With the basic differences in mind, it’s time to focus on what really matters: comparing the total cost of leasing versus buying. Many Albanian buyers make the mistake of comparing just the monthly payment, which is like comparing two restaurant meals by looking only at the appetizer price.

A true apples-to-apples comparison requires you to account for every cost category across the full ownership or lease period. Here’s a structured breakdown:

| Cost category | Leasing | Buying |

|---|---|---|

| Upfront cash | Lower (1st month + fees) | Higher (down payment + taxes) |

| Monthly payments | Lower | Higher |

| Finance charges | Embedded in lease factor | Explicit APR on loan |

| Depreciation risk | Borne by lessor | Borne by buyer |

| Mileage/wear penalties | Potentially significant | None |

| Residual value exposure | None (return the car) | Market-dependent on sale |

| Asset at end of term | None | Vehicle with resale value |

| Opportunity cost of cash | Lower (less tied up) | Higher (more capital deployed) |

For a proper financial comparison, you need to run the numbers. Established calculators model both leasing and buying using inputs like APR, lease interest rate, depreciation, residual value, fees, and upfront cash, giving you a true total cost for each path. This is far more reliable than relying on dealership math.

How to approach the calculation step by step:

- Gather the lease quote: monthly payment, capitalized cost (vehicle price in the lease), residual value, money factor (the lease interest rate), and all fees.

- Gather the loan quote: vehicle price, down payment, loan APR, and loan term in months.

- Add all acquisition costs (taxes, registration, insurance) for both scenarios.

- Project total cash outlay over the same period for both. For buying, subtract the estimated resale value at the end of the lease comparison period.

- Factor in mileage: how many kilometers do you actually drive per year? Multiply your excess by the penalty rate.

- Input everything into a reliable auto loan calculator or lease-vs-buy calculator and compare the net totals.

Pro Tip: Run the calculation twice. Once with your realistic mileage estimate, and once with a figure 25% higher. Albanian roads and driving habits can push annual mileage up significantly, especially for buyers outside major urban centers. If the numbers swing dramatically in the high-mileage scenario, buying is probably the safer financial bet.

For more context on financing structures, the complete car financing guide covers Albanian-specific considerations. And if you’re already thinking about the purchase side, the buying a car in Albania guide walks through the process in detail.

Step-by-step: Deciding for Albanian car buyers

Having clarified how to compare costs, let’s walk through the exact steps Albanian buyers should take when making their choice. While most decision frameworks are written with Western European or North American markets in mind, the same logic applies locally. As international sources remain the strongest mechanically for the lease-vs-buy framework, the key is adapting those inputs to Albanian pricing, mileage norms, and available financing terms.

Step 1: List your actual usage needs

Be honest. How many kilometers do you drive per year? Is this your daily commute car, a family vehicle, or a second car used occasionally? Do you need to carry equipment for work? How long do you plan to keep the vehicle? If your answers point to high mileage, long ownership, or heavy use, buying is almost always more practical.

Step 2: Calculate total upfront and recurring costs using local rates

Don’t rely on advertised rates. Ask the dealership for a written breakdown of all fees. In Albania, additional costs like customs duties on imported vehicles, registration fees, and road tax can add meaningfully to the total upfront cost for buying. Leases may or may not include these depending on the contract.

Step 3: Scrutinize the contract’s fine print

This step alone can change your decision. Look specifically for:

- The annual mileage allowance and per-kilometer penalty

- Wear-and-tear definitions and how they’re assessed at return

- Early termination conditions and associated fees

- Whether the lease includes any purchase option at term end and at what price

Step 4: Apply a calculator and stress-test your assumptions

Input your real numbers. Then change them. Treat the decision as a horizon-based total-cost problem that accounts for upfront cash, finance charges, depreciation or residual risk, fees, mileage penalties, and opportunity cost of capital. Ask: what if the car depreciates faster than assumed? What if you drive 20% more than planned?

Step 5: Make your decision based on your time horizon and priorities

If you want to drive a new car every two to three years, always have warranty coverage, and prioritize lower monthly payments over long-term asset building, leasing can work. If you plan to keep the car for five or more years and want to build equity while avoiding contract constraints, buying wins on total cost in most realistic scenarios.

“The smartest car decision isn’t the one with the lowest monthly payment. It’s the one where the total cost over your actual ownership period fits your financial goals.”

For additional context on navigating purchases safely, check out the buying used cars in Albania guide.

Troubleshooting and common mistakes to avoid

Once you’ve gone through the comparison and decision steps, it’s critical to avoid mistakes that often catch buyers off guard. These aren’t rare edge cases. They’re the most common traps Albanian car buyers fall into, and they’re entirely avoidable with the right preparation.

Mistake 1: Focusing only on monthly payments

When dealers advertise lower monthly payments for leases, the key nuance is that monthly payment isn’t the whole story: you typically have mileage and wear terms, and you may end with no vehicle equity. A lease payment of 20,000 ALL per month looks great until you realize that over three years you’ve paid 720,000 ALL and own nothing.

Mistake 2: Skipping the fine print on mileage and wear

Mileage overage fees are where lease contracts make up for their low monthly rates. A contract that charges 0.05 EUR per excess kilometer sounds small until you’ve driven 8,000 kilometers over the limit. That’s 400 EUR extra at contract end, sometimes more. If you want lower complexity and lower risk of contract-end surprises, prioritize reading the lease’s fine print: mileage allowance, wear-and-tear charges, disposition fees, and what happens if market value differs from the residual assumption.

Mistake 3: Misunderstanding equity

Buyers sometimes assume that after paying monthly lease fees for three years, they’ve built up some form of financial credit toward the next car. That’s not how leases work. Unless your contract includes a purchase option that you exercise, you end the lease with zero equity and start fresh.

Mistake 4: Ignoring early termination risk

Life changes. Jobs change. Family situations change. If you need to exit a lease early due to financial hardship or a change in circumstances, the termination fees can be severe. Some contracts require you to pay all remaining monthly payments regardless.

Pro Tip: Always ask the dealer to show you the full payoff schedule at months 12, 24, and 36. This tells you exactly what it would cost to exit early and helps you evaluate real flexibility before signing.

Common questions to ask before finalizing any lease or purchase are covered thoroughly in essential questions for car financing. And for first-time buyers in Albania, the car buying tips for beginners guide offers practical, local context, while the car buying and selling guide covers the full transaction process.

“Signing a lease without reading the mileage and wear-and-tear clauses is like agreeing to a rental contract without checking the damage deposit terms. The surprise almost always costs money.”

Our perspective: Lease vs buy in Albania isn’t a one-size-fits-all answer

After everything we’ve seen in the Albanian car market, one pattern stands out clearly: buyers who regret their lease decision almost always made it based on the monthly payment figure alone. They didn’t run the total cost, they didn’t stress-test the mileage assumptions, and they didn’t read the fine print before signing.

The “lower monthly payment” narrative that leasing dealers use is mathematically accurate but financially incomplete. Yes, your monthly outgoing is lower. But you’re also paying to use an asset you’ll never own, and if you consistently lease every three years, you’re in a perpetual payment cycle with no equity accumulation. Over a 10-year period, a buyer who purchases and keeps a reliable vehicle will almost always come out significantly ahead in net worth terms compared to someone who leased continuously.

That said, leasing isn’t irrational. For buyers who genuinely value driving a newer, warranty-covered vehicle without the hassle of resale, and who drive predictable, moderate annual mileage, leasing can be a reasonable lifestyle choice. The Albanian market is also seeing more competitive lease options as local dealerships expand their financing partnerships, which means terms are improving. You can explore the evolving landscape through our breakdown of leasing pros and cons in the Albanian context.

Our honest take: for the majority of Albanian buyers, especially those outside Tirana who tend to drive longer distances, buying a reliable used or new vehicle with a loan and keeping it for five or more years is the financially superior path. But the right answer depends on your usage, your priorities, and your willingness to engage with the contract details. The calculator doesn’t lie. Run it, stress-test it, and let the numbers tell you what the monthly payment comparison won’t.

Explore your options with CarPulse

You’ve worked through the framework. Now it’s time to put it into practice.

CarPulse is Albania’s dedicated car marketplace, where you can browse hundreds of new and used vehicle listings filtered by make, model, year, price, mileage, and fuel type. Whether you’re leaning toward buying your next car outright or evaluating dealership lease offers, CarPulse connects you directly with verified dealerships and private sellers who can give you real, comparable options. If you already own a vehicle and want to upgrade, you can sell your car quickly through the platform using VIN-based listing that auto-fills all the details. The CarPulse mobile app for iOS and Android keeps the entire process accessible wherever you are, making your next car decision simpler and more informed.

Frequently asked questions

Is leasing or buying a car more cost-effective in Albania?

Leasing typically carries lower monthly payments, but buying builds equity and can be far more cost-effective long-term if you keep the car after it’s fully paid off.

How do mileage limits affect leasing in Albania?

Lease contracts include set mileage allowances, and exceeding those limits triggers per-kilometer penalties at contract end, which can add up to significant unexpected costs.

What are the key inputs for lease-vs-buy calculators?

The most critical inputs are APR or lease money factor, residual value and depreciation, upfront cash, monthly fees, expected mileage, and any end-of-term charges.

Can I negotiate contract terms for leasing in Albania?

Yes. Before signing, you can negotiate the mileage cap, upfront payment amount, end-of-term purchase option price, and penalties. Reading the lease fine print carefully before those conversations puts you in a much stronger position.