Guides

How to finance a car in Albania: your complete guide

How to finance a car in Albania: your complete guide

TL;DR:

- Albanian buyers have multiple car financing options including bank loans, deposit-collateralized credit, leasing, and dealer partnerships. It’s important to consider total repayment costs, not just interest rates, when choosing a financing method. Preparing necessary documents and comparing offers from different lenders can help secure the best deal.

Buying a car in Albania is exciting until you start asking how to actually pay for it. High upfront costs, confusing loan terms, and a growing market for electric vehicles leave many buyers stuck before they even visit a dealership. The good news is that Albanian buyers have more financing paths than most people realize, including bank consumer loans, deposit-collateralized credit, leasing, and dealer partnerships. This guide walks you through every option, what you need to qualify, and how to avoid the traps that cost buyers thousands of lekë more than necessary.

Table of Contents

- Understanding car financing options in Albania

- Preparing to finance: Requirements and documents

- Step-by-step process for securing car financing

- Verifying the true cost: Interest, fees, and resale considerations

- What most Albanian car buyers overlook about financing

- Find your perfect car and financing partner with CarPulse

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Multiple financing options | Loans, leasing, and dealer partnerships provide flexible paths for Albanian car buyers. |

| Prepare key documents | Income proof, deposits, and credit checks are standard requirements from most lenders. |

| Total cost matters most | Always calculate all fees, interest, and long-term expenses before signing any contract. |

| EVs offer long-term savings | Electric vehicles can reduce maintenance costs by up to 80% but need careful charging and resale planning. |

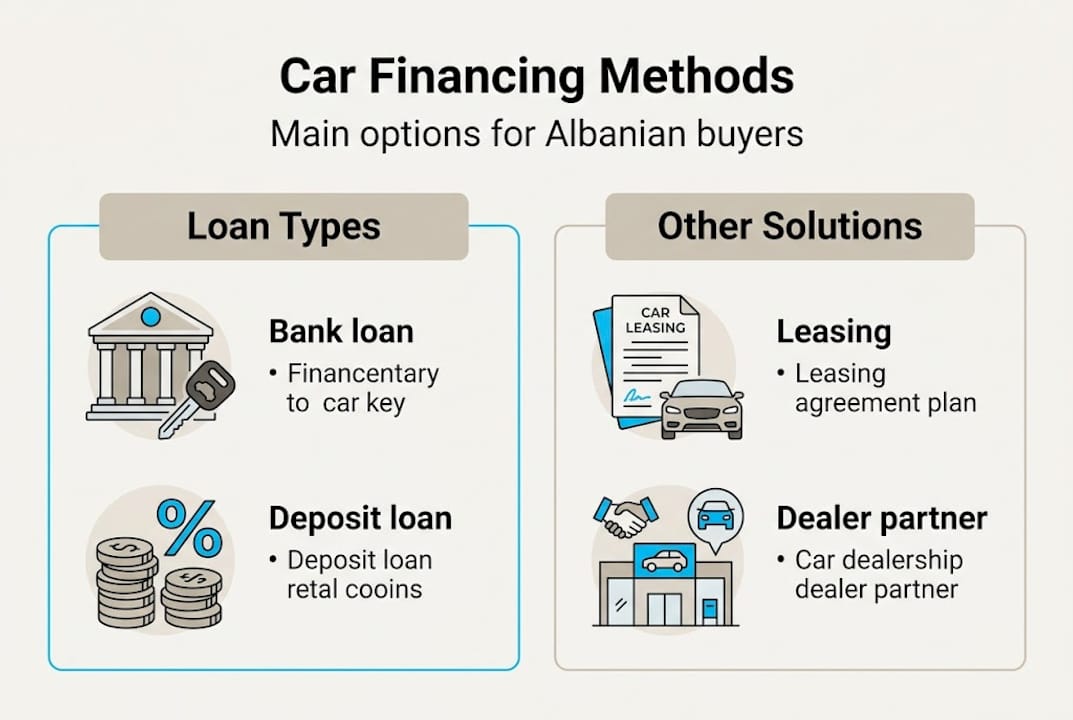

Understanding car financing options in Albania

The Albanian car financing market has grown significantly in recent years, and buyers now have real choices. Understanding each option before you walk into a bank or dealership gives you negotiating power and protects your wallet.

Bank consumer loans are the most common path. You borrow a fixed amount, repay it in monthly installments over an agreed term, and the car is yours from day one. The interest rate depends on your income, credit history, and whether you offer collateral.

Deposit-collateralized loans work differently. Instead of pledging the car or property, you place a cash deposit (often in a term account) as security. This often unlocks lower interest rates because the bank’s risk drops. It is a smart move if you have savings you do not want to liquidate but still want favorable terms.

Leasing is growing fast in Albania. You essentially rent the vehicle for a fixed period, pay monthly fees, and either return it or buy it at the end. Raiffeisen leasing leads the market with 26.33 million EUR financed in 2024, of which 89% was vehicle leasing. ProCredit is another strong player, especially for businesses. Leasing works well if you want lower monthly payments and plan to upgrade every few years.

Dealer financing partnerships connect you directly with a bank or leasing company through the showroom. Convenience is the main benefit, but you should still compare the dealer’s offer against what you could get independently.

For electric vehicles, Albanian buyers can finance EVs through consumer loans, deposit-collateralized credit, leasing, and dealer programs, just like conventional cars. The difference is that some banks offer preferential business terms for EVs. For more context on how these options stack up, our car financing guide breaks down the full picture.

| Financing type | Ownership | Best for | Key watch-out |

|---|---|---|---|

| Bank consumer loan | Immediate | Most buyers | Total cost including fees |

| Deposit-collateralized | Immediate | Savers seeking low rates | Deposit tied up during term |

| Leasing | End of term or return | Frequent upgraders | Mileage and condition limits |

| Dealer partnership | Immediate | Convenience seekers | May not be the cheapest rate |

Always check the total repayment amount, not just the advertised interest rate. Processing fees, annual account fees, and early repayment penalties can add 1 to 2% or more to your real cost.

With this grounding in the bigger picture, let’s break down exactly what you’ll need before you take action.

Preparing to finance: Requirements and documents

Banks and leasing companies in Albania want to know two things: can you repay the loan, and what happens if you cannot? Your documents answer both questions.

Here is what you will typically need:

- Proof of identity — national ID card or passport

- Proof of income — last three to six months of bank statements and salary slips, or a business income declaration if self-employed

- Employment verification — a letter from your employer or business registration documents

- Vehicle documents — registration certificate, technical inspection report, and for imports, customs clearance papers

- Collateral documentation — if using a deposit-collateralized loan, the bank will need proof of the deposit account

For imported vehicles from the USA or other non-EU countries, leasing is a practical alternative to outright purchase, and personal bank loans or credit cards are common tools for covering import costs. Businesses financing EVs often access preferential terms that individual buyers do not.

| Document | New car | Used car | EV | Imported car |

|---|---|---|---|---|

| ID or passport | Required | Required | Required | Required |

| Bank statements | Required | Required | Required | Required |

| Vehicle registration | From dealer | From seller | From dealer | After customs |

| Customs clearance | Not needed | Varies | Not needed | Required |

| Deposit proof | If applicable | If applicable | If applicable | If applicable |

Your credit score matters more than many Albanian buyers expect. A clean repayment history on past loans or credit cards signals reliability and can unlock better rates. If your credit history is thin, starting with a smaller personal loan and repaying it on time builds your profile before you apply for a larger car loan.

Pro Tip: If you are saving for a deposit, place it in a high-interest term account (certificate of deposit) at least three months before applying. Some banks actually accept this account as collateral, so your savings work twice: earning interest and securing a lower loan rate.

Our full buyer’s guide covers additional documentation nuances, and if you are comparing private sellers to dealerships, the section on buying cars in Albania is worth reading before you commit.

Once you have these requirements ready, you are prepared to compare your choices and start the actual process.

Step-by-step process for securing car financing

Knowing your options is one thing. Moving through the process efficiently is another. Here is how it works in practice.

- Set your budget first. Before contacting any bank, calculate the maximum monthly payment you can comfortably afford. A common rule is to keep total car costs (loan, insurance, fuel) under 20% of your monthly income.

- Get at least three offers. Contact UBA, ProCredit, Raiffeisen, and at least one other lender. Comparing total costs across banks including fees and penalties is the only way to find the real winner. Do not stop at the interest rate headline.

- Submit your application. Provide all documents in one go to avoid delays. Incomplete applications are the most common reason for slow approvals.

- Await credit review. Most Albanian banks complete initial reviews within three to seven business days. Leasing companies can sometimes move faster.

- Review the contract carefully. Read every clause, especially the penalty section. Late payment penalties can reach up to 2% of the outstanding balance per occurrence.

“Penalties for late payments can be up to 2% of the outstanding loan amount. Always build a one-month payment buffer in your account before the loan starts.”

- Sign and collect your vehicle. For new cars, delivery may take additional days if the model is not in stock. For used cars, transfer of ownership happens at the notary.

Pro Tip: Dealerships often run seasonal promotions in spring and autumn, bundling free insurance, extended warranties, or reduced processing fees. Timing your purchase around these windows can save you a meaningful amount without any negotiation required.

For used car purchases, our guide on buying a used car safely covers the extra checks you need before signing anything. And if you are also planning to sell your current vehicle, the buying and selling guide explains how to time both transactions to avoid being left without a car or cash.

With financing secured, it is smart to think ahead about the real costs you will face, especially for EVs and used cars.

Verifying the true cost: Interest, fees, and resale considerations

The monthly payment figure on a financing offer is almost never the full story. Here is how to calculate what you will actually pay.

Your real borrowing cost includes:

- Principal (the loan amount)

- Total interest over the full term

- Processing fee (typically 1 to 2% of the loan amount, paid upfront)

- Annual account maintenance fees

- Late payment penalties (up to 2% per occurrence)

- Early repayment fees if you want to pay off the loan ahead of schedule

A loan advertised at 6% annual interest with a 2% processing fee on a 10,000 EUR vehicle costs you significantly more than a 7% loan with no fees, depending on the term. Always ask the lender for the total repayment figure in writing.

Electric vehicle cost factors deserve special attention. EVs typically cost about 80% less in maintenance compared to combustion engine vehicles because there are no oil changes, fewer brake replacements, and simpler drivetrains. Models like the BYD with a 610 km range make long-distance driving realistic. However, resale value depends heavily on battery health and how fast the technology evolves.

Used cars from private sellers can be 15 to 20% cheaper than equivalent dealer stock. That gap is real money, but it comes with less protection. Always verify the vehicle history and have a mechanic inspect it before signing.

For EV leasing or rentals, mileage limits (often 150 to 250 km per day) work perfectly for urban commuters but require planning for road trips. If you drive long distances regularly, factor in charging infrastructure along your routes before committing to an EV.

Our dealership guide helps you evaluate showroom offers critically, and if you are considering a specific brand like Fiat, the Fiat car buying tips article covers brand-specific financing nuances.

Now that you know what you will truly pay and save, let’s see what industry insiders wish buyers would consider before they sign any contract.

What most Albanian car buyers overlook about financing

Most buyers walk into a bank focused on one number: the interest rate. That is understandable, but it is also the reason many people overpay by hundreds or even thousands of euros over the life of a loan.

The smarter move is to negotiate the total cost of the loan, not just the rate. Ask the lender to show you the full repayment schedule with every fee included. Then compare that final number across lenders. A bank offering a lower rate but higher fees often costs more in total.

Deposit-collateralized loans are consistently underused by individual buyers. If you have savings, pledging them as collateral can unlock rates that beat any headline offer, without you losing access to the money permanently.

For electric vehicles, the calculus is more nuanced. The lower maintenance costs are real and significant. But the upfront premium and Albania’s still-developing charging network mean EVs reward buyers who do their homework on routes and charging access before committing.

Advanced buyers also compare direct import financing against dealer financing before deciding. Importing directly from auction can save money on the vehicle price, but the financing structure is different and the paperwork is heavier. Our breakdown of car loans vs. leasing covers this comparison in detail for buyers ready to go deeper.

Find your perfect car and financing partner with CarPulse

Once you know your financing path, the next step is finding the right vehicle at the right price. That is exactly what CarPulse Albania is built for.

CarPulse is Albania’s dedicated car marketplace, where you can filter listings by make, model, fuel type, price, and mileage, including a growing selection of electric vehicles. Verified dealerships and private sellers list side by side, so you can compare dealer financing offers against private sale prices in real time. If you are ready to move on from your current car, you can sell your car directly through the platform with VIN-based listing that fills in vehicle details automatically. The CarPulse mobile app for iOS and Android keeps your search moving wherever you are.

Frequently asked questions

Can I finance a used car in Albania, or is it only for new vehicles?

Yes, you can finance both new and used cars in Albania. Bank loans, leasing, and dealer programs all apply to used vehicles, though lenders may require a vehicle inspection for older models.

What deposit is typically required for car financing?

The deposit amount varies by lender and vehicle type. Collateral loans require a deposit as security, while standard consumer loans may not, though a larger down payment often improves your rate.

Are there special financing conditions or incentives for electric vehicles in Albania?

Individual EV incentives are limited in Albania. ProCredit offers up to 100% EV financing for businesses, but personal buyers mainly benefit through dealership promotions and lower long-term maintenance costs.

How do I compare car loan offers from different banks?

Never compare interest rates alone. Raiffeisen leads the leasing market with 26.33 million EUR financed in 2024, but the best deal for you depends on total repayment including all fees and penalties across every lender you approach.

Recommended

- Financimi i Automjeteve në Shqipëri: Kredi & Leasing |… | CarPulse Albania

- Financimi i automjeteve në Shqipëri: Kredi & Leasing |… | CarPulse Albania

- Blej Makina në Shqipëri: Udhëzuesi i Plotë | CarPulse.al | CarPulse Albania

- Makina ne Shitje Shqipëri - Udhëzuesi i Plotë për Blerje | CarPulse Albania