Guides

Electric Car Leasing Explained: Your 2026 Guide

Electric Car Leasing Explained: Your 2026 Guide

TL;DR:

- Leasing an electric vehicle allows drivers to avoid depreciation and technology obsolescence risks while enjoying lower monthly payments. Most leases last 24 to 48 months, with predictable costs for mileage overages and wear charges, and they provide an easy upgrade path to newer models. For most drivers in 2026, leasing offers a more cost-effective and flexible way to access advanced EV technology.

Electric car leasing is defined as a fixed-term agreement where you pay monthly to use a new electric vehicle without owning it, covering depreciation and finance charges rather than the full purchase price. This structure makes leasing the dominant way Americans access new EVs: 58% of new EV transactions in Q2 2025 were leases, not purchases. That figure reflects a real shift in how drivers think about electric vehicles. When technology changes this fast, paying for temporary use often beats paying for permanent ownership.

What is electric car leasing and how does it work?

Electric car leasing, known in the industry as a closed-end lease or consumer vehicle lease, is a contract between you and a finance company. You pay to use the car for a set period and mileage. At the end, you return it, buy it at a predetermined price, or start a new lease on a different model.

Standard EV lease contracts run 24–48 months with annual mileage caps around 12,000 miles. Excess mileage fees typically run about $0.25 per mile over that cap. A driver who exceeds the limit by 5,000 miles over a three-year lease would owe roughly $1,250 at return. That is a predictable cost, but only if you plan for it.

Monthly payments break down into two components: depreciation and a finance charge. Depreciation is the difference between the car’s starting value and its projected residual value at lease end. The finance charge is calculated using a money factor, which is the leasing equivalent of an interest rate. Multiplying the money factor by 2,400 gives you the approximate APR, which makes it easy to compare lease financing against a traditional auto loan.

Most EV leases also carry acquisition fees at signing and a disposition fee when you return the car. Wear and tear charges apply if the vehicle comes back with damage beyond normal use. Warranty coverage from the manufacturer typically runs the full lease term, which means mechanical repairs are rarely your financial problem.

Pro Tip: Ask the dealer for the money factor in writing before signing. Dealers can legally mark it up, and even a small increase compounds significantly over a 36-month term.

What are the financial benefits and costs of leasing an electric car?

Leasing costs less per month than buying. Average lease payments run about $175 less per month than traditional auto loan payments as of Q2 2025. Over a 36-month lease, that gap adds up to $6,300 in savings compared to financing the same vehicle. Lower monthly payments also mean a lower barrier to entry for drivers who want a premium EV without a large loan.

The financial case for leasing gets stronger when you factor in depreciation. EVs lose 40–50% of their value in the first three years. A buyer who finances a $50,000 EV and sells it after three years could walk away with far less equity than expected. A lessee never faces that loss because the finance company absorbs the depreciation risk. You pay for the use, not the decline in value.

Battery replacement is the hidden financial risk most buyers underestimate. Battery replacement costs on older EVs can exceed £7,000 for some models. Leasing keeps you inside the manufacturer warranty window, so that cost never lands on you. This is one of the most concrete financial protections leasing offers, and it rarely gets enough attention.

There are real costs to watch for, though. Excess mileage fees, end-of-lease wear charges, and gap insurance add up if you are not careful. Gap insurance covers the difference between what you owe on the lease and the car’s actual value if it is totaled. Many leases include it, but not all. Check before you sign.

- Confirm the mileage cap matches your actual annual driving distance before agreeing to any lease term.

- Calculate the true APR by multiplying the money factor by 2,400 and compare it to current auto loan rates.

- Check for included gap insurance in the lease contract so you are not paying for it twice through your auto insurer.

- Ask about disposition fees upfront. These typically run $300–$500 and are due at lease end if you do not buy or re-lease.

- Review wear and tear standards in writing. Each lessor defines acceptable condition differently, and knowing the standard early saves money later.

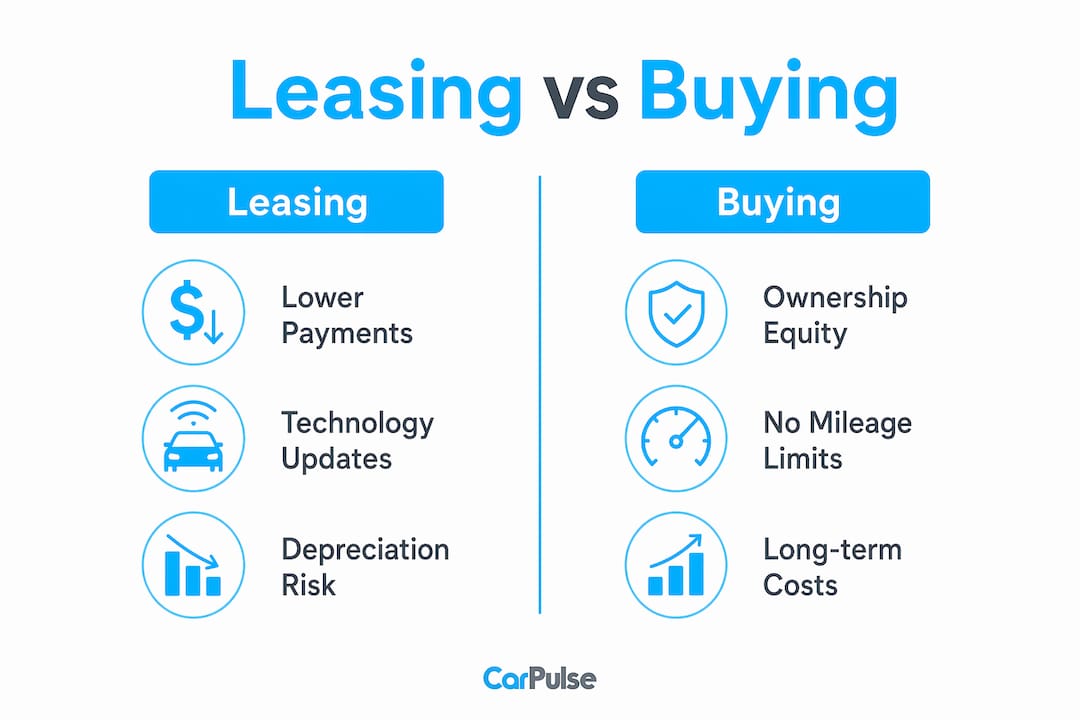

Leasing vs. buying an electric vehicle: which makes more sense?

The core difference between leasing and buying an EV is who absorbs the financial risk of ownership. A buyer takes on depreciation, battery degradation, and technology obsolescence. A lessee transfers all three to the finance company.

Leasing helps drivers avoid technological obsolescence by enabling frequent upgrades to newer models with better battery range and charging standards, according to Consumer Reports. This matters more for EVs than for gas vehicles because the technology gap between a 2023 model and a 2026 model is significant. Battery chemistry, charging speed, and software capabilities have all improved substantially in three years. A lessee can step into that newer technology at lease end without selling anything.

Buying makes more sense in specific situations. Drivers who put on high annual mileage, say 20,000 or more miles per year, will face steep excess mileage fees under a standard lease. Drivers who plan to keep a vehicle for eight or more years also benefit more from ownership, since the per-year cost of a purchase drops significantly over time. And buyers who want to modify their vehicle, from tinting windows to installing aftermarket charging equipment, cannot do that freely under most lease agreements.

Pro Tip: If you drive more than 15,000 miles per year, negotiate a higher mileage cap at signing rather than paying per-mile penalties at the end. Upfront mileage costs less than excess mileage fees.

The equity argument for buying is real but often overstated. Because EVs depreciate so fast, the equity you build in the first three years is modest. You can explore how depreciation affects EV buyers in the Albanian market specifically, where EV adoption grew 12% in 2026. The pattern holds broadly: rapid depreciation erodes the ownership advantage faster than most buyers expect.

For drivers who prioritize lower monthly costs, access to the latest technology, and predictable expenses, leasing is the stronger choice. For drivers who value ownership, plan to drive heavily, or want to customize their vehicle, buying wins.

How to choose and manage an electric vehicle lease effectively

Choosing the right lease starts with an honest look at your driving habits. Pull your last 12 months of odometer readings and calculate your true annual mileage. Most drivers underestimate this number, which leads to mileage penalties at lease end.

Once you know your mileage, focus on these steps when evaluating electric vehicle lease options:

- Match the lease term to your technology tolerance. A 24-month lease gives you faster access to new models. A 48-month lease lowers monthly payments but locks you in longer as EV technology advances.

- Negotiate the capitalized cost. This is the agreed selling price of the vehicle, and it directly affects your monthly payment. Dealers often treat it as non-negotiable, but it is not.

- Understand the residual value. A higher residual value means lower monthly payments. It also means the buyout price at lease end will be higher, which matters if you are considering purchasing the car.

- Check for battery health guarantees. Many EV leases include battery health clauses that protect you if capacity drops below a certain threshold during the lease term. Confirm this is in your contract.

- Plan your lease-end strategy early. Decide at month 30 of a 36-month lease whether you will return, buy, or re-lease. This gives you time to get a pre-inspection 30–60 days before lease end and fix any damage affordably before the lessor charges for it.

Understanding car battery lifespan also helps you maintain the vehicle in good condition throughout the lease, reducing the risk of wear charges tied to battery-related components. For a broader look at how leasing fits into vehicle financing, the vehicle financing guide on Carpulse covers loan and lease structures in detail.

Key Takeaways

Electric car leasing is the most cost-efficient way to access new EV technology in 2026, transferring depreciation and battery risk to the finance company while keeping monthly payments well below loan costs.

| Point | Details |

|---|---|

| Lower monthly payments | Lease payments average $175 less per month than auto loans, saving over $6,000 across a 36-month term. |

| Depreciation protection | EVs lose 40–50% of value in three years; leasing shifts that financial loss to the finance company. |

| Battery risk transfer | Leasing keeps you under warranty, avoiding battery replacement costs that can exceed £7,000 on older models. |

| Technology flexibility | Returning a lease every 2–4 years lets you upgrade to better range, faster charging, and improved software. |

| Mileage planning is critical | Excess mileage fees of $0.25 per mile add up fast; match your cap to your actual driving habits before signing. |

Why I think leasing is the right default for most EV drivers right now

The conventional wisdom says leasing is for people who “always want something new.” That framing misses the real reason leasing makes sense for EVs specifically. The financial risk of owning an EV in a market where battery chemistry and software are still evolving rapidly is genuinely high. Buyers are not just accepting depreciation. They are accepting the possibility that their car becomes functionally outdated before the loan is paid off.

I have seen drivers lock into five-year loans on EVs that were genuinely competitive at purchase and noticeably behind the market by year three. The resale math rarely works out the way buyers expect. Leasing is not about vanity. It is about not betting on a technology curve you cannot predict.

The one caveat I would give is this: if you drive heavily and your lifestyle does not fit a 12,000-mile annual cap, leasing requires careful negotiation. High-mileage drivers should either negotiate a higher cap upfront or look at leasing pros and cons carefully before committing. The penalty structure can erase the monthly savings quickly if you are not disciplined about it.

For most drivers in 2026, though, leasing an EV is the financially sound choice. The technology is moving too fast to own.

— Henri

Carpulse makes it easier to find EV lease deals in Albania

Carpulse is Albania’s largest online car marketplace, and it lists both new and used electric vehicles from verified dealerships across the country. If you are ready to compare current electric vehicle lease options, the platform lets you filter by fuel type, price, and mileage so you can find deals that match your budget and driving habits.

Browsing electric vehicles on Carpulse takes minutes, and the VIN-based listing system means every vehicle detail is accurate before you contact a seller. Whether you are comparing lease terms from multiple dealerships or looking for your first EV, Carpulse gives you the full picture in one place. The mobile app for iOS and Android keeps your search active wherever you are.

FAQ

What is the typical length of an electric car lease?

Most EV leases run 24–48 months, with 36 months being the most common term. Shorter leases offer faster access to newer technology, while longer terms lower the monthly payment.

How are monthly lease payments calculated?

Lease payments cover the vehicle’s depreciation over the lease term plus a finance charge based on the money factor. Multiply the money factor by 2,400 to convert it to an approximate APR for easy comparison.

What happens if I exceed my mileage limit?

Excess mileage fees typically run about $0.25 per mile over the cap. A 5,000-mile overage on a standard lease would cost around $1,250 at return.

Is leasing an electric car worth it compared to buying?

Leasing is worth it for drivers who want lower monthly payments, protection from EV depreciation of 40–50% in three years, and the ability to upgrade to newer technology every few years. Buying makes more sense for high-mileage drivers or those planning to keep the vehicle long-term.

Can I buy the electric car at the end of my lease?

Yes. Most closed-end EV leases include a buyout option at a price set at the start of the contract. If the car’s market value exceeds that residual price at lease end, buying can be a strong financial move.

Recommended

- Financimi i automjeteve në Shqipëri: Kredi & Leasing |… | CarPulse Albania

- Financimi i Automjeteve në Shqipëri: Kredi & Leasing |… | CarPulse Albania

- Blerja e Makinave Online në Shqipëri: Rritja e EV-ve 2026 | CarPulse Albania

- Blerja e makinave online në Shqipëri: Rritje 12% e EV në… | CarPulse Albania