Guides

Car insurance in Albania: Coverage, costs, and smart protect

Car insurance in Albania: Coverage, costs, and smart protection

TL;DR:

- Many Albanian drivers mistakenly believe that purchasing the cheapest insurance policy provides full protection, risking significant financial loss.

- Mandatory third-party liability insurance only covers damages caused to others, not your own vehicle or injuries.

Many Albanian car owners assume that buying the cheapest available policy means they’re fully protected. That assumption is understandable, but it can lead to serious financial pain. The gap between what minimum insurance covers and what you actually need is wider than most people realize. With car insurance prices rising in 2026, understanding exactly what you’re paying for has never been more important. This guide breaks down mandatory coverage, optional protections, cross-border rules, and real costs so you can make a confident, informed decision.

Table of Contents

- What is mandatory car insurance (TPL) in Albania?

- Going beyond the basics: Casco and optional coverages

- Understanding cross-border driving: The Green Card system

- How much does car insurance cost in Albania?

- What most Albanian drivers overlook about car insurance

- Get the most value from your next car purchase

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Minimum required | Mandatory TPL covers only third-party harms, not your own vehicle or injuries. |

| Optional protection | Casco and similar insurance provide financial security for your own car against multiple risks. |

| Cross-border travel | A Green Card is essential for driving outside Albania and requires fast accident reporting for claims. |

| Evolving costs | Insurance prices are rising in Albania, with new factors influencing rates in 2026 and beyond. |

| Smart decisions | Matching insurance coverage to your risk and driving habits ensures better financial protection. |

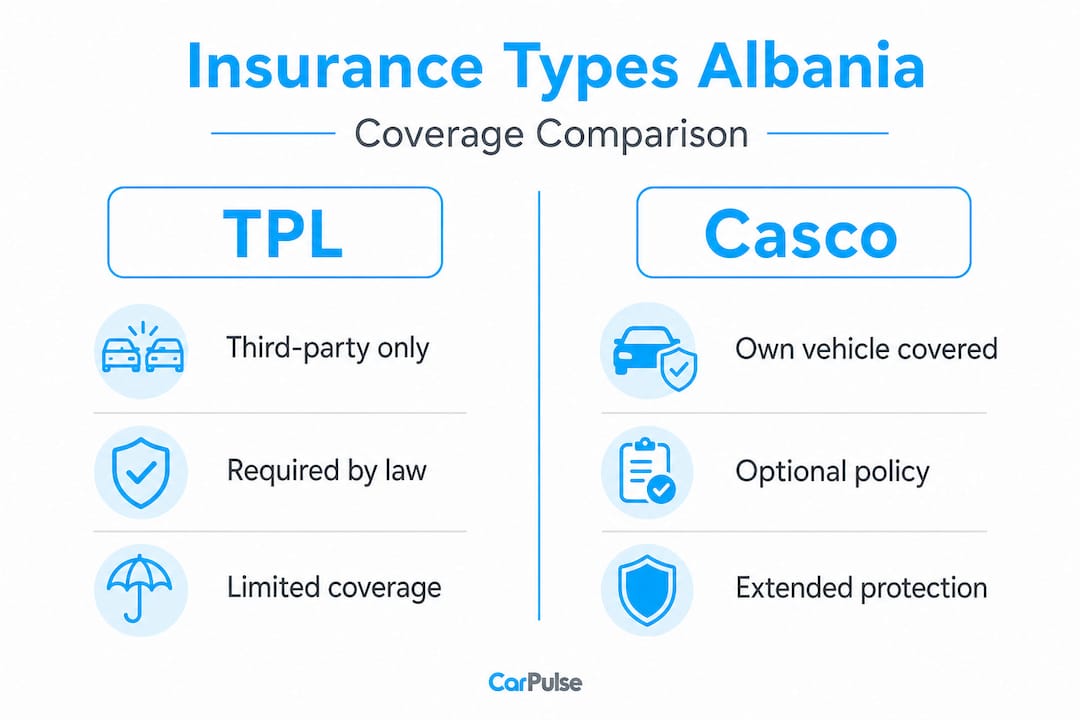

What is mandatory car insurance (TPL) in Albania?

Every car on Albanian roads must carry a minimum form of insurance. There are no exceptions, and ignorance of the law is not a defense. Before you decide whether to buy extra coverage, you need to understand precisely what the legal minimum does and does not do for you.

Third-party liability insurance (known as TPL or MTPL) is the mandatory minimum motor insurance for all vehicles circulating in traffic within Albania. The word “third-party” is the key here. TPL is designed to protect other people, not you. If you cause an accident and injure someone else or damage their property, your TPL policy steps in to pay those costs.

Specifically, TPL indemnifies third-party harms including death, disability, health injuries, and material and property damage. But here is the critical detail that trips up most drivers: it does not cover damage to the driver or vehicle that caused the event. In plain terms, if you rear-end another car and the fault is yours, your policy pays for their repairs and medical bills. Your own car sits in the lot with a crumpled hood at your expense.

Understanding third-party warranty benefits can help you frame exactly why this type of coverage exists and why it was designed the way it was. The system is built around compensating victims, not at-fault drivers.

What happens if you drive without TPL?

The consequences of operating a vehicle without valid TPL coverage are significant:

- Heavy fines issued by traffic police during routine stops

- Possible vehicle impoundment until proof of insurance is provided

- Full personal financial liability for any damage or injuries you cause

- Inability to renew your vehicle registration

- Legal exposure if an injured third party pursues civil claims against you

Pro Tip: Do not assume your old policy auto-renews. Many Albanian drivers are caught driving on a lapsed policy simply because they forgot to check the expiration date. Set a reminder in your phone one month before your policy ends, every single year.

Real cost scenario: A driver without TPL causes a moderate accident injuring one person and damaging a vehicle valued at 800,000 lekë. Without insurance, every lekë of that liability comes directly out of their own pocket, plus legal costs if the case escalates.

Going beyond the basics: Casco and optional coverages

Once you know what’s required, the next question is whether basic protection is really enough. For many drivers in Albania, it simply is not.

Car owners considering more-than-minimum protection in Albania commonly look at Casco variants, including Kasko and Minicasco, which insure damage to the vehicle itself in addition to third-party exposure. These are optional products, but calling them “extras” undersells how much they matter in practice.

Casco (sometimes spelled Kasko) is full comprehensive vehicle insurance. It protects your car against a broad range of risks. Minicasco is a lighter version that covers a selected subset of those risks, typically at a lower premium.

Core risks that Casco covers

- Theft of the vehicle or its parts

- Damage from road accidents, regardless of fault

- Fire and explosion

- Natural disasters including flooding, hail, and falling trees

- Vandalism and intentional damage by third parties

- Collision with animals

Coverage-selection nuance matters here: if you rely only on mandatory TPL, you remain exposed to costs for damage to your own vehicle. A hailstorm, a stolen side mirror, a tree branch that falls on your hood — none of those are TPL events. They are your personal financial problem unless you have Casco.

TPL vs Casco vs Minicasco: A side-by-side comparison

| Coverage feature | TPL | Casco | Minicasco |

|---|---|---|---|

| Third-party injury | ✓ | ✓ | ✓ (via bundled TPL) |

| Third-party property damage | ✓ | ✓ | ✓ (via bundled TPL) |

| Your own vehicle damage | ✗ | ✓ | Partial |

| Theft | ✗ | ✓ | Often included |

| Fire and natural disasters | ✗ | ✓ | Sometimes included |

| Vandalism | ✗ | ✓ | Rarely included |

| Cost | Lowest | Highest | Mid-range |

Who benefits most from Casco or Minicasco?

If you are financing or leasing a vehicle, your lender will almost certainly require Casco as a loan condition. Check out this vehicle financing guide to understand why lenders insist on full coverage and how it affects your total cost of ownership. If you own a newer or higher-value car outright, Casco is still worth serious consideration because the repair or replacement costs for modern vehicles are substantial. For older, lower-value cars, Minicasco may offer the right balance.

When evaluating any coverage, it helps to understand warranty coverage examples from real car owners to appreciate how gap in protection can create real financial exposure.

Pro Tip: Even the most careful driver in Albania cannot control hailstorms, flooding, or another driver slamming into a parked car. TPL leaves all of those risks on your shoulders. The relevant question is not “am I a good driver?” but “can I afford to replace my car out of pocket?”

If fuel efficiency is a factor in your purchase decision, our fuel efficient car picks can help you narrow down models worth insuring comprehensively. And once you own a vehicle, following solid car maintenance tips can reduce wear-related claims and potentially keep future premiums lower.

Understanding cross-border driving: The Green Card system

But what if you travel outside Albania? Here’s where coverage gaps can create real headaches.

Green Card insurance is mandatory for Albanian-registered vehicles traveling outside Albania to countries within the Council of Bureaux system. It covers civil liability to third parties for incidents occurring abroad. The Green Card is not a separate physical insurance product in every case; it is often an extension or endorsement added to your existing motor policy, but you must confirm it is active before crossing any border.

The Council of Bureaux network covers most of Europe including EU member states, and several neighboring countries in the Balkans and beyond. If you drive from Tirana to North Macedonia, Greece, or Italy for a vacation, your Albanian TPL alone is not sufficient. You need the Green Card to be covered for third-party liability claims in those countries.

What drivers must do after an accident abroad

- Stop immediately and secure the scene safely

- Contact local emergency services if anyone is injured

- Exchange insurance details with the other party, including their insurer name and Green Card number

- Document everything: photos of damage, vehicle positions, license plates, and road conditions

- Notify your Albanian insurer within 24 hours of the incident

That last point is critical. Notification within 24 hours is generally required when using Green Card coverage for damages that occurred outside Albania. Missing that window can jeopardize your entire claim. It does not matter if you are on a highway in northern Italy with limited phone service. You need to find a way to contact your insurer within that timeframe.

| Step | Action required | Time limit |

|---|---|---|

| 1 | Stop and secure the scene | Immediate |

| 2 | Call emergency services if needed | Immediate |

| 3 | Collect third-party info and document damage | At the scene |

| 4 | Notify your Albanian insurer | Within 24 hours |

| 5 | Submit formal claim documentation | Per insurer requirements |

If you are exploring the idea of importing cars from Germany or elsewhere in Europe, understanding cross-border insurance obligations is an essential first step before that vehicle ever hits Albanian roads.

Pro Tip: Before any trip abroad, call your insurer and ask two specific questions. First: “Is my Green Card active and valid for the countries I’m visiting?” Second: “What is the exact 24-hour notification number I should call if I have an accident?” Save that number in your phone before you leave.

How much does car insurance cost in Albania?

With the coverage types clear, let’s turn to a question on every car owner’s mind: what will it actually cost?

Prices in Albania have been shifting upward. Compulsory policy prices now average around 19,500 lekë, and January 2026 saw a 7% rise attributed to a new system for determining compulsory vehicle insurance premiums, with broader factor-based impacts expected throughout 2026. That means budgeting for insurance based on last year’s numbers could leave you short.

Main factors that affect your insurance price in Albania

- Vehicle age and value: Newer or higher-value vehicles carry higher premiums, especially for Casco

- Engine size and power: Larger engines typically mean higher risk ratings

- Driver history: Past claims and traffic violations directly influence your premium

- Geographic area: Urban drivers in Tirana face different risk profiles than rural drivers

- Coverage type selected: Adding Casco or Green Card to a TPL base significantly increases total cost

- The new rating system: Albania’s updated pricing model uses more granular risk factors, which means two seemingly similar drivers can now receive meaningfully different quotes

For optional coverages, costs vary widely. A full Casco policy for a mid-range vehicle in good condition might add 30,000 to 60,000 lekë or more annually on top of your TPL premium. Minicasco sits somewhere in the middle depending on which risks are included. Green Card coverage for European travel is often a relatively modest add-on if your base policy already covers third-party liability, but you must request it explicitly.

The practical takeaway is straightforward: factor insurance into your total ownership budget before you buy a car, not after. A vehicle that seems affordable at the purchase price can become expensive to operate once you add mandatory TPL, appropriate optional coverage, and the fuel and maintenance costs that come with any car.

What most Albanian drivers overlook about car insurance

Having explored costs and rules, let’s pull back for an honest reality check: what do most people in Albania get wrong about car insurance?

The first and most common mistake is treating TPL as real protection. It is not protection for you. It is protection for the person you might hurt. Confusing the two is a costly error. Drivers who pay the minimum and feel “covered” are actually exposed to every risk that involves their own vehicle, their own health, and their own financial loss.

The second blind spot is cross-border complacency. Many Albanian drivers take weekend or vacation trips to Greece, North Macedonia, or Montenegro without confirming their Green Card status. They assume that because they have insurance, they are covered everywhere. They are not. Green Card coverage is required for Albanian-registered vehicles traveling outside Albania in Green Card member countries, and correct territorial coverage is essential for any claim to succeed abroad. One fender-bender in Greece without a valid Green Card could mean paying tens of thousands of lekë out of pocket.

The third mistake involves claims timing. Many drivers, especially those involved in accidents abroad or in complex situations at home, wait too long to notify their insurer. They gather information, they talk to people, they sleep on it. And in doing so, they blow past notification windows that can invalidate an entire claim.

“The most expensive insurance mistake isn’t buying too much coverage. It’s finding out too late that what you bought doesn’t cover what just happened to you.”

The practical principle here is simple: buy insurance for your actual risk profile, not just for the legal requirement. If you drive a newer vehicle, live in an urban area with heavy traffic, or travel outside Albania regularly, minimum coverage is not adequate. Follow maintenance tips for Albanian roads to keep your vehicle in good shape, but also keep your insurance in the same condition: updated, confirmed, and matched to how you actually use your car.

Get the most value from your next car purchase

Armed with a real understanding of coverage, costs, and obligations, you are now in a much stronger position to make smart decisions about the vehicles you buy and the insurance you carry.

At CarPulse, Albania’s online car marketplace, you can browse thousands of new and used vehicle listings filtered by make, model, year, price, mileage, and fuel type. When you know what a vehicle costs to insure before you buy it, you can factor that into your decision from the start rather than discovering surprises later. Whether you’re researching your next vehicle or ready to sell your car and upgrade, CarPulse connects you with verified dealerships and private sellers in one place. The VIN-based listing system ensures every vehicle’s details are accurate, so you can trust what you’re reading. Make your next move with the full picture in hand.

Frequently asked questions

Do I need insurance if my car is not used daily?

Yes. Albanian law requires TPL insurance for all registered vehicles in use, regardless of how frequently you drive. As long as the vehicle is registered and circulating in traffic, coverage is legally mandatory.

Does TPL insurance protect me if I damage my own vehicle?

No. TPL covers third-party harms only, including injuries and property damage to others. Any damage to your own vehicle requires Casco or an equivalent optional coverage on top of TPL.

What should I do after a car accident abroad with Green Card coverage?

Document the accident fully, exchange insurance details, and notify your insurer within 24 hours for damages that occurred outside Albania. Missing that notification window can invalidate your claim entirely.

Why did car insurance prices in Albania rise in 2026?

A new risk-based pricing system took effect, leading to a 7% increase in January for compulsory premiums, with the average policy now around 19,500 lekë. Further adjustments tied to expanded risk factors are expected throughout the year.