Guides

Car financing explained: your guide to smart auto purchases

Car financing explained: your guide to smart auto purchases

TL;DR:

- Albania offers diverse car financing options including bank loans, non-bank loans, leasing, and cash purchases.

- Understanding key terms like NEI, principal, interest rate, and collateral is essential when comparing loans.

- Negotiating rates, increasing down payments, and comparing multiple offers can save buyers significant money.

Buying a car in Albania is exciting until the financing conversation starts. Many buyers assume you need perfect credit, a large salary, or a long relationship with a major bank just to qualify for a loan. That assumption leaves a lot of people either overpaying in cash when they don’t have to, or walking away from a deal they could have secured. The reality is that the Albanian lending market has expanded significantly, with both bank and non-bank options now available to a wider range of buyers. This guide breaks down every option, every key term, and every step so you can walk into any lender’s office with confidence.

Table of Contents

- Understanding car financing basics

- Comparing financing options in Albania

- The step-by-step process to secure your car loan

- Smart tips for getting the best deal

- Why most buyers overlook the true cost and how to avoid it

- Find your ideal car and financing in one place

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your options | Car financing in Albania includes banks, non-bank lenders, and leasing each with unique benefits and costs. |

| Check the NEI rate | Always compare the full NEI—not just the advertised interest rate—to understand true borrowing costs. |

| Document readiness | Gather ID, proof of income, and purchase details before you apply for a smooth approval process. |

| Negotiate and compare | Shop multiple lenders, check collateral advantages, and always negotiate for the best deal. |

Understanding car financing basics

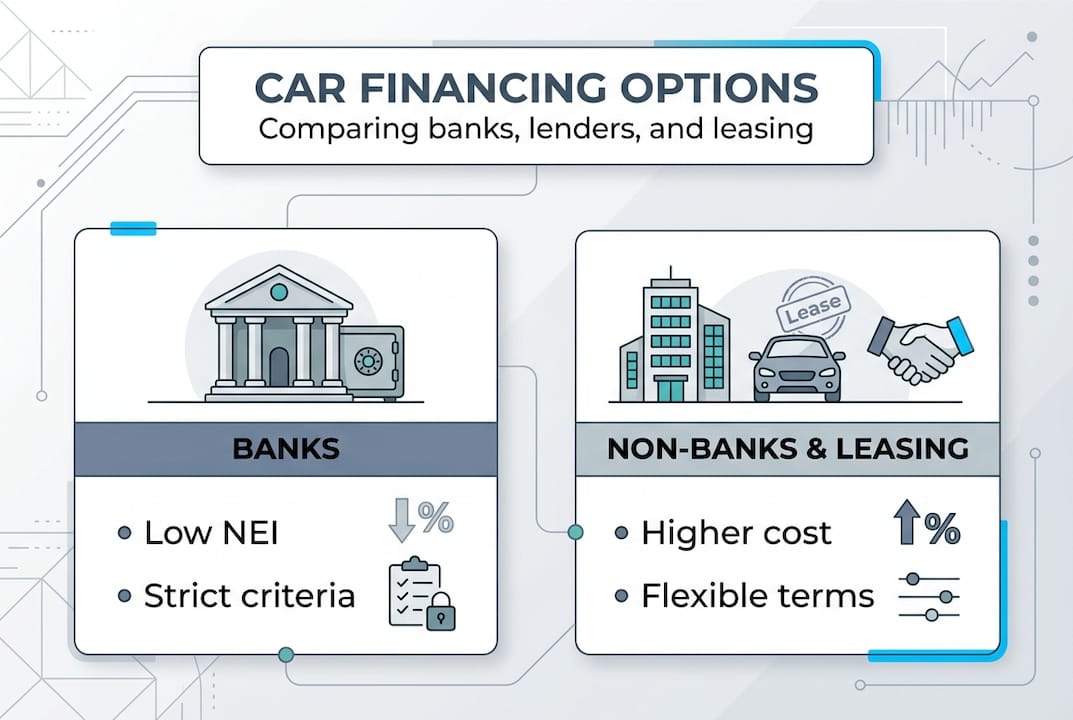

Car financing simply means borrowing money to buy a vehicle and paying it back over time, usually with interest. Instead of handing over the full purchase price upfront, you agree to a structured repayment plan. In Albania, this takes three main forms: traditional bank loans, non-bank personal loans, and leasing arrangements.

Before you compare any offers, you need to know the terms lenders will throw at you:

- Principal: The amount you actually borrow, not counting interest.

- Interest rate: The percentage the lender charges on your principal each year.

- Loan term: How many months you have to repay the loan.

- NEI (Norma Efektive e Interesit): The effective annual interest rate, which includes all fees and charges, not just the base interest. This is the number that tells you the real cost of your loan.

- Down payment: The upfront amount you pay out of pocket before the loan kicks in.

- Collateral: An asset (like property or a savings deposit) you pledge to the lender as security.

For a broader look at how these pieces fit together, the vehicle financing overview on CarPulse is a solid starting point.

One of the biggest misconceptions in Albania is that non-bank lenders are risky or unregulated. That’s not accurate. Non-bank financial institutions operate under Albanian law and are supervised by the Bank of Albania. In fact, non-bank loans up to 600,000 ALL for up to 60 months are available and can be used directly for car purchases, repairs, or related services, with NEI reaching up to 54.65% for higher-risk profiles.

Typical eligibility requirements across most lenders include:

- Proof of steady income (employment contract or business documentation)

- Valid Albanian ID

- A minimum down payment, often 10 to 30% of the vehicle’s value

- Collateral for larger loan amounts or lower rates

- A clean or acceptable credit history

Keep in mind: NEI is the single most important number to compare across lenders. Two loans with the same interest rate but different fees can have very different NEI values, and the one with the higher NEI will cost you more in total.

The complete financing guide on CarPulse walks through each option in detail if you want to go deeper after reading this.

Comparing financing options in Albania

Now that you understand the basics and terminology, let’s examine how the different car financing routes compare.

| Financing type | Typical NEI | Loan amount | Term | Collateral needed |

|---|---|---|---|---|

| Bank loan | 6% to 14% | Up to 5,000,000 ALL | Up to 84 months | Often required |

| Non-bank loan | Up to 54.65% | 20,000 to 600,000 ALL | 2 to 60 months | Not always required |

| Leasing | Varies | Based on vehicle value | 12 to 60 months | Vehicle itself |

| Cash purchase | N/A | N/A | N/A | N/A |

Bank loans generally offer the lowest NEI, but they come with stricter approval criteria. You’ll typically need a strong income history, a good credit record, and often collateral. If you qualify, a bank loan is usually the most affordable way to finance a car over the long term.

Non-bank lenders fill the gap for buyers who don’t meet bank requirements. The tradeoff is cost. Non-bank NEI rates can reach up to 54.65% for higher-risk borrowers, which means you pay significantly more over the life of the loan. However, the approval process is faster, documentation requirements are lighter, and collateral is often optional.

Leasing works differently. You’re essentially renting the vehicle for a fixed period, with an option to buy at the end. Monthly payments are usually lower than a traditional loan because you’re not paying off the full vehicle value. But you don’t own the car during the lease, which affects insurance, modifications, and mileage limits.

Cash purchases give you the most negotiating power. Sellers, especially private ones, are often willing to drop the price for an immediate, no-financing deal. If you can pay cash, you also avoid all interest costs entirely.

Collateral changes everything. For example, deposit-collateral financing at UBA offers rates as low as the deposit interest rate plus 2%, which is one of the most affordable structures available. Pledging a savings deposit as collateral dramatically lowers your rate and improves your approval odds.

Pro Tip: If you’re on the fence between a bank and a non-bank loan, apply to both simultaneously. Approval decisions often come faster than expected, and having two offers lets you negotiate.

For a side-by-side breakdown of the two most common routes, the car loans vs. leasing in Albania guide covers the key differences in plain terms.

The step-by-step process to secure your car loan

Once you’ve compared your options, it’s time to act. Here’s how to go from application to driving away.

- Set your budget first. Before approaching any lender, know your maximum monthly payment and total loan amount. Factor in insurance, registration, and maintenance.

- Choose your lender type. Based on your credit profile and income, decide whether a bank, non-bank, or leasing company fits best.

- Gather your documents. Most lenders require: valid ID, proof of income (payslips or tax returns), a signed car purchase agreement or proforma invoice, proof of address, and collateral documentation if applicable.

- Submit your application. Non-bank lenders often process applications online within 24 to 48 hours. Banks may take longer.

- Review the loan offer carefully. Check the NEI, total repayment amount, monthly installment, and any early repayment penalties.

- Sign and finalize. Once you accept, funds are disbursed directly to the seller or dealership in most cases.

- Register the vehicle. Complete the ownership transfer and insurance before driving.

Here’s a real example of what a non-bank loan actually costs. A 300,000 ALL loan over 60 months at 34.09% NEI results in a monthly payment of approximately 9,361 ALL. That means you’ll pay roughly 561,660 ALL in total, meaning about 261,660 ALL in interest over five years.

| Loan amount (ALL) | Term (months) | NEI | Monthly payment (ALL) | Total repaid (ALL) |

|---|---|---|---|---|

| 150,000 | 36 | 34.09% | ~6,200 | ~223,200 |

| 300,000 | 60 | 34.09% | ~9,361 | ~561,660 |

| 500,000 | 60 | 20% | ~13,200 | ~792,000 |

Pro Tip: Always ask the lender for the total repayment figure, not just the monthly payment. That single number tells you exactly how much the car is really costing you.

The step-by-step car loan process and the Albania car buying guide on CarPulse are both worth bookmarking before your first lender meeting.

Smart tips for getting the best deal

With your car loan offer in hand, here’s how to make sure you’re really getting the best value and not overpaying over time.

Watch for hidden fees. Lenders sometimes charge application fees, file processing costs, mandatory insurance add-ons, or early repayment penalties. Always ask for a full fee schedule before signing anything.

Negotiate before you commit. The interest rate, loan term, and upfront fees are often negotiable, especially if you have a competing offer. Lenders want your business. A lower NEI of even 2 to 3 percentage points can save you tens of thousands of ALL over a 48 or 60 month term.

Use collateral strategically. If you have a savings deposit, property, or another asset, pledging it as collateral can unlock significantly better rates. This is especially true at traditional banks.

Increase your down payment. A larger upfront payment reduces your principal, which lowers both your monthly payment and total interest. Even an extra 50,000 ALL upfront can meaningfully reduce your total cost.

Here are the most common pitfalls first-time buyers in Albania fall into:

- Focusing only on the monthly payment without checking the total repayment amount

- Skipping the fine print on insurance requirements tied to the loan

- Accepting the first offer without getting at least one competing quote

- Underestimating ongoing costs like fuel, maintenance, and registration renewals

Key stat: NEI rates for higher-risk profiles can reach up to 54.65%, meaning a 300,000 ALL loan could cost you nearly double over five years if you’re not careful about which product you choose.

Pro Tip: Use an online loan calculator before your first lender meeting. Plug in different NEI values and terms to see how the total cost changes. It takes five minutes and can save you years of overpaying.

The car buying market tips guide on CarPulse also covers negotiation tactics specific to the Albanian market.

Why most buyers overlook the true cost and how to avoid it

Here’s the uncomfortable truth: most car buyers in Albania focus almost entirely on the monthly payment. It’s understandable. A number like 9,000 ALL per month feels manageable. But that focus can blind you to the full picture.

When you only look at the monthly installment, you’re ignoring how much you’re actually paying for the car over its entire loan life. A loan with a slightly lower monthly payment but a longer term or higher NEI can cost you 200,000 ALL more than a better-structured loan.

The real opportunity is before you sign. Negotiating the NEI down by even 1 percentage point, shortening the term by 12 months, or eliminating a processing fee can each save meaningful money. Most buyers never try because they assume the offer is fixed. It rarely is.

Getting two or three competing offers before committing is the single most effective thing you can do. Walk into a lender with a better offer in hand, and you’ll often see rates move. Don’t be afraid to walk away. There are enough lenders in Albania now that walking away from one deal usually means a better one is available.

The complete buying and selling guide on CarPulse covers this negotiation mindset in depth, and it’s worth reading before you start any serious conversations with lenders or dealers.

Find your ideal car and financing in one place

Ready to compare real deals and find the car that’s right for you? CarPulse makes it easier to move from research to decision without bouncing between a dozen websites.

On the CarPulse marketplace, you can browse hundreds of new and used vehicle listings filtered by make, model, year, price, mileage, and fuel type. Verified dealerships and private sellers both list on the platform, so you get a real picture of what’s available and at what price. Alongside the listings, CarPulse publishes updated financing guides tailored to the Albanian market, so you can match the right car to the right loan structure before you ever contact a seller.

Frequently asked questions

What documents do I need to apply for a car loan in Albania?

Most lenders require a valid ID, proof of income, a car purchase agreement, and in some cases collateral documentation or proof of address. Requirements vary slightly between banks and non-bank lenders.

Can I get a car loan in Albania without collateral?

Yes. Non-bank lenders offer loans up to 600,000 ALL without requiring collateral, though borrowers with higher-risk profiles will face higher NEI rates.

How is the NEI different from the simple interest rate?

NEI represents the total annual cost of borrowing, including all fees and charges, not just the base interest rate. It’s the most accurate number to use when comparing loan offers from different lenders.

What’s the typical loan amount and term for financing a car in Albania?

Non-bank loans typically range from 20,000 to 600,000 ALL with terms between 2 and 60 months, depending on your income and risk profile.