Guides

Car Depreciation Explained: What Every Buyer Must Know

Car Depreciation Explained: What Every Buyer Must Know

TL;DR:

- Car depreciation is the reduction in a vehicle’s value over time, mainly due to age, mileage, and market demand. Buying a used car from two or three years ago helps buyers avoid the steepest depreciation losses of new cars.

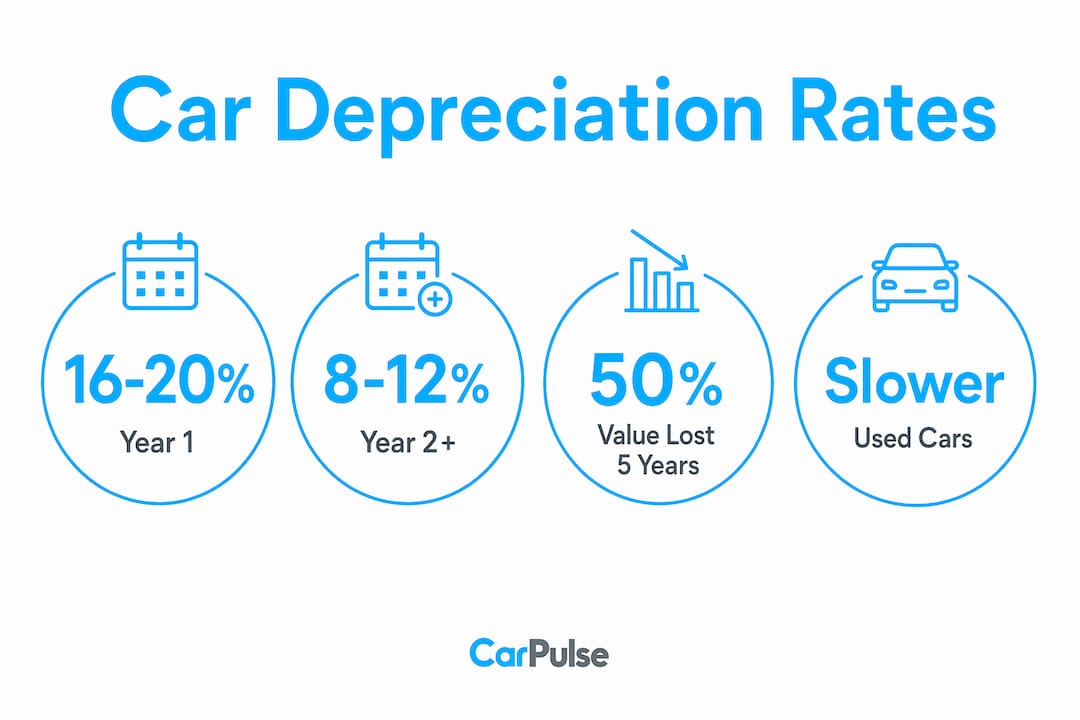

Car depreciation is defined as the decline in a vehicle’s monetary value from its purchase price over time, driven by age, mileage, and market demand. For anyone buying a car, depreciation is the single most important financial factor to understand before signing anything. New cars lose roughly 20% of value in the first year alone, and around 60% by year five. That means a $30,000 car could be worth $12,000 five years later, regardless of how carefully you drive it. Understanding vehicle depreciation before you buy protects your budget, shapes your loan decisions, and determines how much you recover when you sell.

What is car depreciation and how does it work?

Car depreciation is the gap between what you paid for a vehicle and what it is worth at any point after purchase. The industry term is “asset depreciation,” and it applies to cars the same way it applies to computers or machinery. The moment you drive a new car off the lot, its value drops. That drop is not a rumor. New cars lose about 10% of their value within the first month of ownership.

Depreciation is not the same as your loan balance. Your loan follows an amortization schedule, meaning you pay down principal and interest on a fixed timeline. Depreciation follows market forces. These two numbers move independently, which creates a real risk: long loan terms of 72–84 months can leave you owing more than the car is worth. That situation is called negative equity, or being “underwater” on your loan.

Several forces drive how fast a car loses value:

- Age: Older vehicles are worth less, regardless of condition.

- Mileage: Higher mileage signals more wear and reduces buyer demand.

- Accident history: A reported collision permanently lowers resale value.

- Market demand: Popular models hold value better than slow sellers.

- Fuel type: Shifts in fuel technology, such as the rise of electric vehicles, can accelerate depreciation for older fuel types.

- Color and trim: Neutral colors and popular trim levels retain value better than rare or polarizing options.

Pro Tip: Check a vehicle’s accident history before buying. A single reported collision can reduce resale value significantly, even if the repair was done perfectly.

What are typical car depreciation rates by year?

Understanding car depreciation rates by year gives you a clear picture of when value drops fastest and when it stabilizes. The pattern is consistent across most vehicle categories.

New cars take the hardest hit early. Depreciation slows to roughly 8–12% annually after year two, but the first two years are brutal. Here is how the numbers typically break down:

| Year | Approximate Depreciation | Cumulative Value Retained |

|---|---|---|

| Year 1 | 16–20% | 80–84% |

| Year 2 | ~12% | ~70% |

| Year 3 | ~11% | ~60% |

| Year 4 | ~9% | ~52% |

| Year 5 | ~7% | ~45–55% |

The table shows something critical: the steepest drop happens before year three. After that, the curve flattens. A five-year-old car loses value much more slowly than a one-year-old car does.

Used cars depreciate more slowly for a simple reason. The first owner already absorbed the biggest loss. When you buy a three-year-old vehicle, you skip the steepest part of the depreciation curve entirely. Buying a 2–3 year old vehicle means the first owner absorbed a 20–30% loss so you do not have to.

Pro Tip: If you plan to sell or trade in within three years, buy used. If you plan to keep a car for ten or more years, the new-car premium matters less because you spread the depreciation cost over a longer period.

Which car brands hold their value best?

Brand reliability is one of the strongest predictors of how well a car holds its value. Reliable brands like Toyota, Honda, and Subaru consistently depreciate more slowly than the industry average. Buyers trust these brands because of their long track records for low repair costs and high longevity. That trust translates directly into stronger resale demand.

Luxury brands tell a different story. A premium German sedan may cost $70,000 new but lose value faster than a $30,000 Japanese sedan. The reason is simple: luxury cars carry higher maintenance costs, which shrinks the pool of buyers willing to purchase them used. Smaller buyer pools mean lower resale prices.

Here is what separates high-retention brands from fast-depreciating ones:

- Repair cost reputation: Vehicles with lower average repair costs attract more used buyers.

- Parts availability: Common vehicles with widely available parts are easier and cheaper to maintain.

- Model consistency: Brands that keep the same model design for several years build stronger used-market recognition.

- Reliability rankings: Vehicles that score well in long-term reliability studies hold value because buyers see them as lower risk.

Factors that affect used car prices go beyond brand alone. Regional demand, fuel type trends, and local market conditions all play a role. A model that holds value well in one market may depreciate faster in another.

Verified car listings help buyers confirm a vehicle’s actual condition and service history, both of which directly affect how much value it retains at resale.

How can buyers reduce the financial impact of depreciation?

The most effective strategy for managing vehicle depreciation is to buy a car that has already absorbed its steepest drop. A two or three-year-old vehicle with low mileage and a clean service history gives you the best balance of price, reliability, and future resale value. You get a nearly new car at a significantly lower cost, and your own depreciation exposure is much smaller.

Follow these steps to protect your money:

- Buy used, not new. Target vehicles that are 2–3 years old. The first owner took the largest hit so you benefit from a lower purchase price and slower future depreciation.

- Choose a reliable brand. Toyota, Honda, and Subaru consistently outperform the market on resale value. Start your search with models known for low ownership costs.

- Keep detailed service records. Well-maintained vehicles command better prices at trade-in and private sale. Every oil change receipt and inspection record adds credibility and value.

- Avoid long loan terms. A 72 or 84-month loan keeps your monthly payment low but increases the risk of negative equity. Depreciation moves faster than long-term amortization schedules.

- Think about resale before you buy. Neutral colors, popular trim levels, and high-demand models are easier to sell and command stronger prices.

- Consider detailing before selling. Professional detailing can boost resale value by presenting the vehicle in its best possible condition to prospective buyers.

Pro Tip: Run a quick resale value check on any car you are considering before you buy it. If the model has a poor resale track record, factor that future loss into your total cost of ownership calculation today.

Key Takeaways

Depreciation is the largest cost of car ownership, and buying a 2–3 year old reliable vehicle is the most effective way to reduce its financial impact.

| Point | Details |

|---|---|

| Depreciation starts immediately | New cars lose roughly 10% of value within the first month of purchase. |

| Steepest drop in years 1–2 | New vehicles lose 16–20% in year one; the rate slows to 8–12% after year two. |

| Used cars are smarter buys | A 2–3 year old car skips the steepest depreciation curve and costs less upfront. |

| Brand reliability matters | Toyota, Honda, and Subaru consistently retain more value than luxury or low-reliability brands. |

| Long loans increase risk | Loan terms of 72–84 months can leave you owing more than the car is worth. |

Depreciation is the cost most buyers never see coming

I have spoken with dozens of car buyers who obsessed over fuel economy and monthly payments but never once calculated what their car would be worth in three years. That gap in thinking is where most of the financial pain comes from.

Depreciation is often the largest ownership cost, surpassing fuel, insurance, and maintenance combined over a typical ownership period. Yet most buyers treat it as an afterthought. They negotiate hard on the sticker price and then ignore the $8,000 in value that evaporates in the first two years.

The mindset shift I recommend is simple: treat every car purchase as a timed financial decision, not just a transportation decision. Ask yourself how long you plan to own the vehicle, what it will likely be worth when you sell, and whether the total cost of ownership fits your actual budget.

Timing matters too. Buying a two-year-old version of a reliable model instead of a new one can save you $5,000 to $10,000 in absorbed depreciation, with very little sacrifice in quality or reliability. That is real money. Depreciation only becomes real when you sell, trade in, or face a total-loss insurance claim. But by then, the decisions that shaped your outcome were made years earlier, at the moment of purchase.

Plan the exit before you sign the entry.

— Henri

Find your next car on Carpulse

Knowing how depreciation works is only half the equation. The other half is finding a vehicle that holds its value and fits your budget from day one.

Carpulse is Albania’s largest online car marketplace, connecting buyers with verified private sellers and dealerships across the country. You can filter listings by make, model, year, mileage, price, and fuel type to zero in on vehicles with strong resale track records. Every listing supports direct seller contact, and the platform’s VIN-based listing system means vehicle details are accurate from the start. Whether you are browsing the full marketplace for your next reliable buy or ready to list your current car for sale, Carpulse gives you the tools to make depreciation work in your favor.

FAQ

What is car depreciation in simple terms?

Car depreciation is the loss of a vehicle’s value over time due to age, mileage, and market conditions. It is the difference between what you paid and what you can sell the car for later.

How much does a new car depreciate in the first year?

New cars typically lose 16–20% of their value in the first year. Within the first month alone, that drop is roughly 10%.

Does depreciation affect my monthly car payment?

Depreciation does not directly change your monthly payment, which is set by your loan terms. However, it affects your equity position, and a fast-depreciating car can leave you owing more than the vehicle is worth.

Which cars depreciate the slowest?

Vehicles from brands with strong reliability reputations, such as Toyota, Honda, and Subaru, consistently depreciate more slowly than the industry average. High demand and low ownership costs drive stronger resale prices.

Is buying a used car better for avoiding depreciation?

Buying a 2–3 year old used car is one of the most effective ways to reduce depreciation losses. The first owner absorbs the steepest drop, so your own value loss from that point forward is much smaller.